{kind=link}

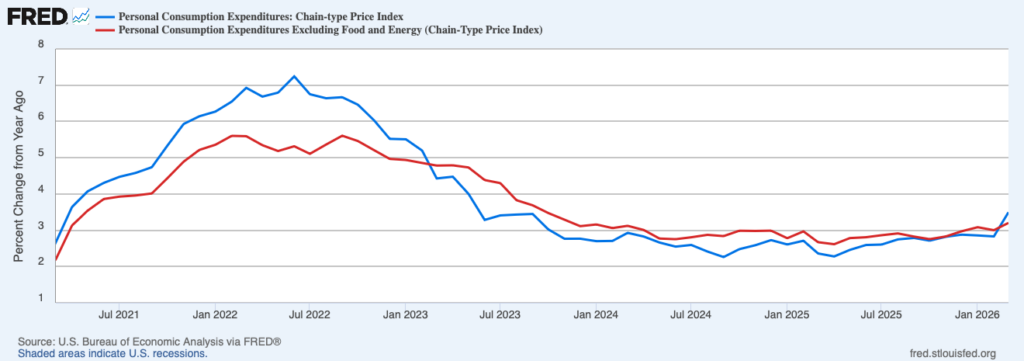

No one will be surprised to hear that inflation has picked up. But new data from the Bureau of Economic Analysis confirms it. The Personal Consumption Expenditures Price Index (PCEPI), which is the Federal Reserve’s preferred measure of inflation, grew at an annualized rate of 8.3 percent in March 2026, up from 4.6 percent in the prior month. The PCEPI grew at an annualized rate of 5.6 percent over the last six months and 3.5 percent over the last year.

Figure 1. Headline and Core Personal Consumption Expenditures Price Index Inflation, March 2021 – March 2026

Much of the observed increase over the last two months is related to the ongoing conflict in the Middle East, which has pushed up energy prices. The price index for energy goods and services grew 11.6 percent in March — or 271.8 percent annualized. The price of energy has grown 14.4 percent over the last year.

High inflation is not limited to the energy sector, however. Core inflation, which excludes food and energy prices and is thought to be a better gauge of the underlying rate of inflation, remains well above the Fed’s longer-run target. Core PCEPI grew at an annualized rate of 3.6 percent in March 2026. It grew at an annualized rate of 3.7 percent over the last six months and 3.2 percent over the last year.

AIER’s Monetary Neutrality Report, released this morning, identifies the primary driver of the broader inflation problem: excess nominal spending growth.

Milton Friedman taught us that “Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.” When the amount of money being spent in an economy grows faster than real output, prices must rise. And when an increase in nominal spending growth is not matched by an increase in real output growth, prices must rise more rapidly. A surge in nominal spending growth, therefore, tends to produce higher inflation.

Nominal spending has surged over the last year. It grew 5.4 percent from 2024:Q4 to 2025:Q4. It grew at an annualized rate of 5.6 percent in 2026:Q1. For comparison, nominal spending grew at an average annualized rate of 4.1 percent over the five years just prior to the pandemic. If real GDP growth averages 2.5 percent, nominal spending growth would need to average around 4.5 percent for the Fed to hit its two-percent inflation target. Hence, at 5.6 percent, nominal spending is growing about 1.1 percentage points faster than the Fed would like.

Taken together, the available evidence suggests inflation is high for two distinct reasons: the ongoing conflict in the Middle East, which disproportionately affects energy prices, and broader inflationary pressures related to excess nominal spending. The energy price hikes are temporary, with energy prices returning to normal when the conflict ends and production resumes. But the broader inflationary pressures related to excess nominal spending imply that the Federal Reserve still has some work to do.

Sadly, many Fed officials have been slow to acknowledge the broader inflationary pressures. They blame the conflict in the Middle East and, before that, tariffs for the uptick in inflation.

At the post-meeting press conference earlier this week, Fed Chair Jerome Powell acknowledged that “Inflation has moved up recently and is elevated relative to our two-percent, longer-run goal.” He said the increase in headline inflation was due to “the significant rise in global oil prices that has resulted from the conflict in the Middle East,” whereas the high core inflation “largely reflects the effects of tariffs on prices in the goods sector.”

The view that tariffs have had a meaningful effect on inflation is difficult to square with the data. Tariffs affect relative prices, to be sure. A 10 percent tariff on automobiles will tend to raise the price of automobiles relative to everything else. But tariffs increase inflation only insofar as they reduce real output growth. But real output growth has been strong. Real GDP grew 2.7 percent over the last year. For comparison, real GDP growth averaged 2.6 percent per year over the five years just prior to the pandemic.

Looking ahead, Powell described the economic outlook as “highly uncertain” and said that “the conflict in the Middle East has added to this uncertainty.” He expects “higher energy prices will push up overall inflation” in the near term, but said “the scope and duration of potential effects on the economy remain unclear, as does the future course of the conflict itself.”

Notably absent from Powell’s remarks is any concern that nominal spending is growing too rapidly. This is especially worrisome given recent Fed mistakes.

In the back half of 2021, Fed officials believed rising inflation was primarily due to pandemic-related supply disruptions, even though the incoming data suggested otherwise. Real GDP had largely recovered. But, rather than returning to trend, prices accelerated. Still, Fed officials clung to the belief that the high inflation was transitory. And, even after they dropped the word transitory and appeared to acknowledge the excess nominal spending problem, they delayed tightening monetary policy. The result was the worst inflationary episode in forty years.

Now, the Fed risks repeating that mistake. In this case, Powell is right that supply disruptions are pushing up prices. But that is only part of the story. The other part — and the part that monetary policy is best-suited to address — is the excess nominal spending, which has largely gone unnoticed.

There is one key difference between then and now, however. This time around, at least some Fed officials are genuinely concerned about high inflation, so much so that they broke ranks with the rest. Three regional Reserve Bank presidents — Beth Hammack (Cleveland), Neel Kashkari (Minneapolis), and Lorie Logan (Dallas) — dissented at this week’s meeting, preferring to remove the easing bias in the FOMC’s post-meeting statement. They will need to persuade their colleagues that the high inflation is broader and more persistent than what we all can see clearly at the pump, and take steps to reduce nominal spending growth.