{kind=link}

“Without tariffs,” the President said on his affordability tour in Georgia, “everybody would be bankrupt, the whole country would be bankrupt.” In court, the Trump administration has made similar sweeping claims, arguing that revoking certain tariff authorities would have “catastrophic consequences” and “lead to financial ruin.”

The Supreme Court has now struck down the administration’s “reciprocal tariffs” imposed under the International Emergency Economic Powers Act (IEEPA). This is a major victory for American consumers and businesses who suffered from higher taxes and higher prices that the tariffs imposed.

And contrary to the President’s claims, tariffs were never going to prevent national bankruptcy. America’s debt crisis does not arise from a revenue problem. The federal government has an unsustainable spending problem.

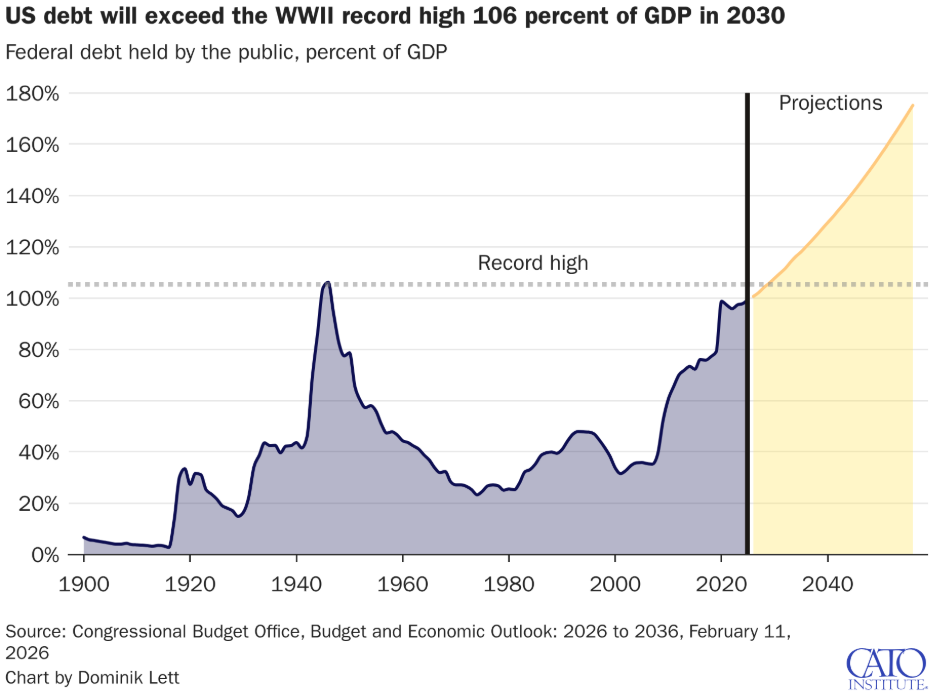

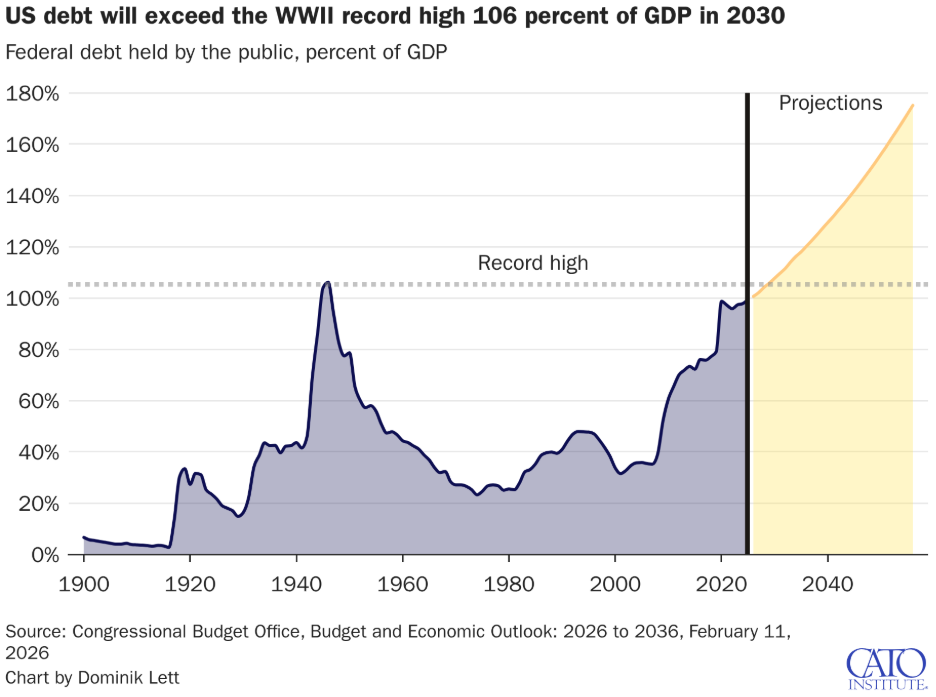

The Congressional Budget Office’s (CBO) latest Budget and Economic Outlook shows debt held by the public exceeding 100 percent of GDP this year and rising past its World War II record by 2030. Ten years from now, debt reaches roughly 120 percent of GDP and continues climbing to 175 percent by 2056 — and that is under optimistic projections that assume no economic, financial, or public health crises over that time frame.

{kind=link}

Revenues are not the problem. Even after extending and adding to the Trump tax cuts, federal receipts are projected to remain near or above their historical average as a share of the economy, growing from $5.2 trillion (17.2 percent of GDP) to $8.3 trillion (17.8 percent of GDP) over the decade.

The problem is that federal spending exceeds revenues by a lot and is growing much faster than revenues. Spending is projected to grow from $7 trillion (23.1 percent of GDP) to $11.4 trillion (24.4 percent of GDP).

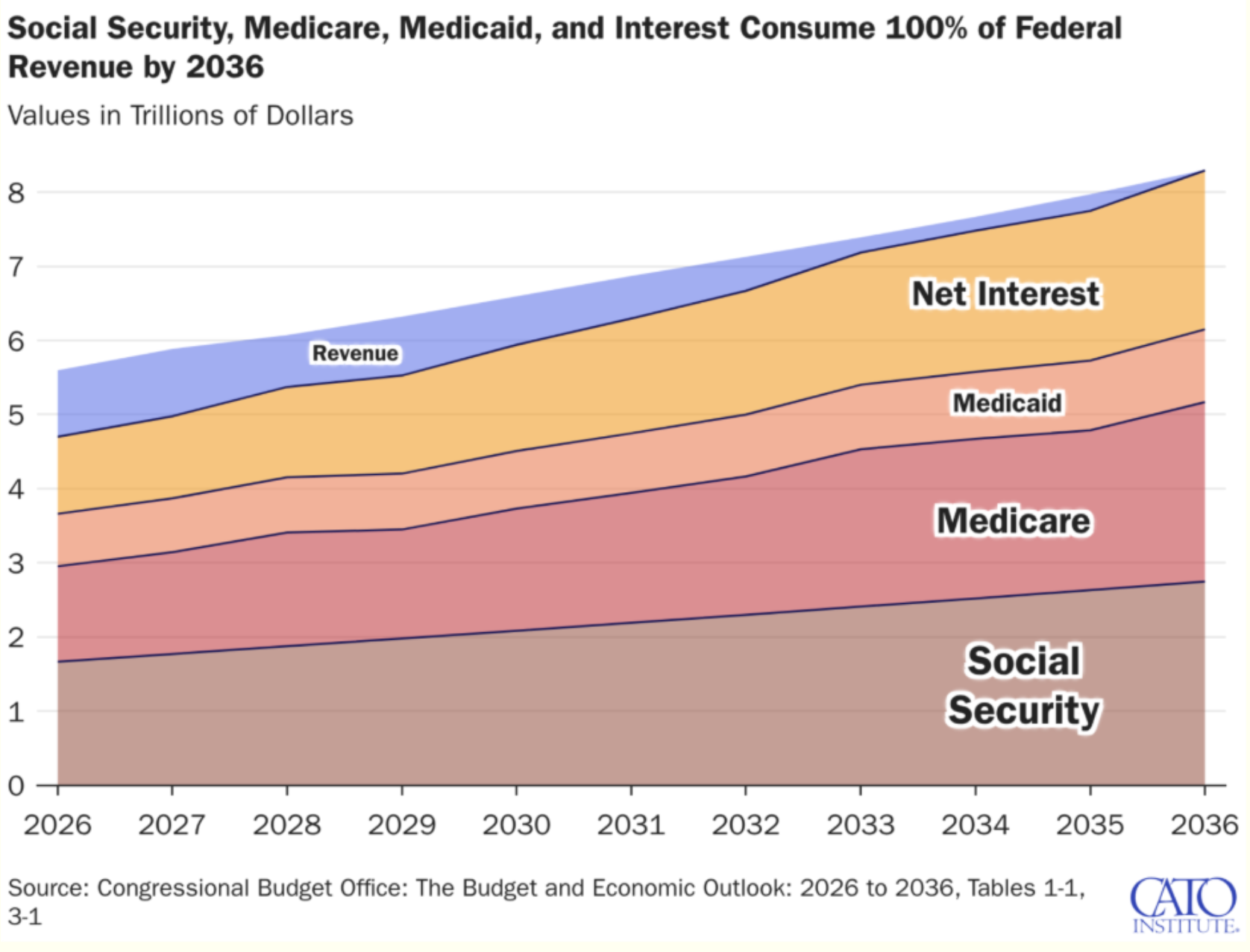

The widening annual deficit (the gap between annual spending and revenue) is overwhelmingly driven by the growth in Social Security, Medicare, Medicaid, and rising interest costs. By 2036, interest costs, Social Security, Medicare, and Medicaid are projected to consume 100 percent of federal revenues.

Read that again.

Under current law, within a decade, every dollar collected in revenue will be absorbed by health care programs, Social Security, and interest spending to service the ballooning federal debt, leaving nothing for national defense or any other core function of government.

Against that backdrop, the claim that revoking tariff authority would produce “financial ruin” or “bankrupt” the country does not withstand scrutiny.

{kind=link}

Multiple estimates, from the Congressional Budget Office, the Yale Budget Lab, the Penn Wharton Budget Model, and the Tax Foundation, estimate that the Trump tariffs would generate from $1 trillion to $3 trillion in additional revenue over a decade, depending on assumptions and whether economic feedback effects are included.

Those are large numbers in isolation. But they are small relative to the size of the federal budget hole.

CBO projects that the United States will borrow an additional $25 trillion over the next decade. Closing that gap would require eight to 25 times the revenues that Trump administration tariffs were estimated to bring in. About $16 trillion of those deficits will go toward interest payments alone. Even under optimistic assumptions, tariff revenue would offset only a small fraction of that amount.

Put differently: even if every dollar of projected tariff revenue materialized, the debt would still surge past its historic high within a few years and continue unsustainably climbing thereafter.

Moreover, tariffs are neither free money nor are they paid by foreign exporters. They function as taxes on imported goods and production inputs that are paid by Americans. According to the Kiel Institute, American consumers and importers paid 96 percent of tariff costs, while foreign exporters absorbed only four percent. Higher input costs reduce business profits and workers’ wages, shrinking corporate and individual income tax collections. From generating uncertainty to reducing available capital for investment, tariffs reduce hiring and dampen economic growth.

Part of the “revenue gain” from tariffs is thus clawed back through weaker economic performance and a smaller tax base. That’s one way to shoot yourself in the foot.

Meanwhile, the real driver of America’s debt trajectory is far more entrenched.

The entirety, more than 100 percent, of the federal government’s long-term funding shortfall stems from the growth of Social Security and Medicare, according to the Financial Report of the United States Government. These programs expand automatically as the population ages, beneficiaries live longer, benefits increase by design, and health costs rise. They were set up for a younger country with far fewer retirees per worker and transfer income from working Americans to retirees, regardless of need. One of the best ways to curb their growth is to refocus these programs’ benefits on seniors in need.

As debt climbs, interest costs compound. CBO projects that net interest will more than double over the next decade, consuming a growing share of the budget.

Interest costs already surpass what the United States government allocates toward national defense expenditures. As the Hoover Institution’s Niall Ferguson writes: “when a great power spends more on debt service than on defense, it will not be great for much longer.” The US Senate unanimously recognized deficits as “unsustainable, irresponsible, and dangerous,” but Congress has yet to act to curb the debt threat.

This is how fiscal crises develop — not because a single revenue stream disappears, but because structural commitments grow faster than the economy that must finance them.

The United States is already well above the debt levels that much of the economic literature associates with slower long-term growth. Every year of delay increases the eventual adjustment required to stabilize the debt.

Congress should adopt a credible plan that stabilizes spending and the growth in debt. Members of the bipartisan fiscal forum in Congress recently proposed a three-percent-of-GDP deficit target, led by Representatives Bill Huizenga (R-MI), Scott Peters (D-CA), Lloyd Smucker (R-PA) and Mike Quigley (D-IL). That’s a promising goal. To succeed in meeting it, Congress will need structural entitlement reforms. Not killing the goose that lays the golden eggs with economy-crushing tax hikes — whether those are dressed up as tariffs or as a border adjustment tax.

Congress can reduce excess health care spending, streamline taxes, and cut welfare programs prone to fraud and abuse, using the same reconciliation process that Republicans leveraged in July to extend and expand the Trump tax cuts and slow the growth in Medicaid and food stamps (SNAP).

Going yet further, Congress can work toward advancing a Base Realignment and Closure–style fiscal commission to overcome policy inertia and provide Congress with political cover to advance necessary entitlement reforms. The Fiscal Commission Act, championed by Representatives Scott Peters (D-CA) and Bill Huizenga (R-MI) is a promising step in that direction.

If America ever experiences fiscal “ruin,” it will not be because presidential tariff authority was constrained. It will be because elected officials of both parties failed to modernize the country’s largest entitlement programs and halt their automatic spending growth.

The Supreme Court’s ruling does not create a fiscal crisis. Tariffs raised revenue at the margin. In the process, they also distort trade and slow growth. But they do not alter the fundamental arithmetic driving America’s debt.

The path to fiscal stability runs through entitlement reform and spending control — not through executive-imposed tariffs that were never large enough to solve the problem in the first place.