{kind=link}

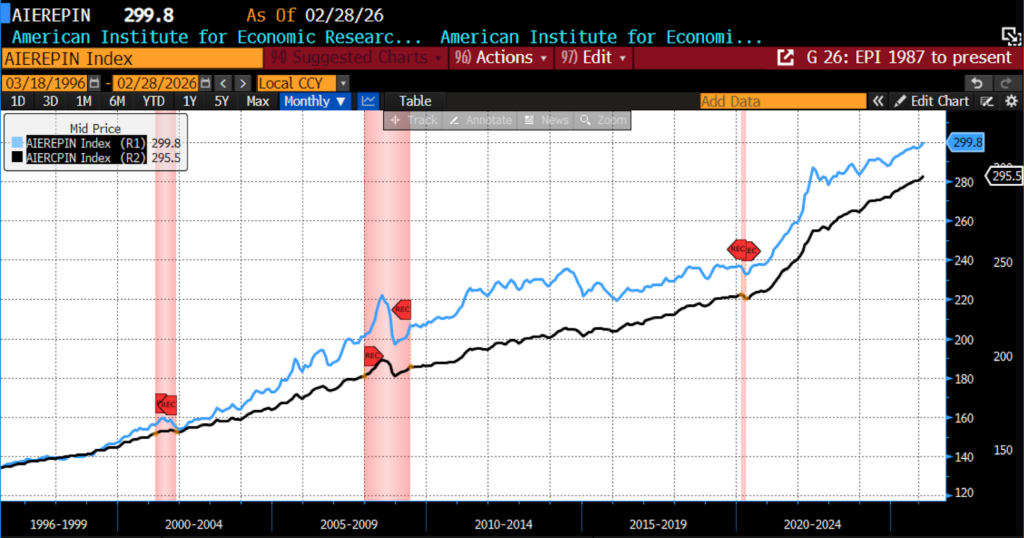

The AIER Everyday Price Index (EPI) saw its largest jump in 13 months in February 2026, rising 0.61 percent to 299.8. This was the index’s fourth largest monthly increase going back two years. Fourteen of the 24 constituents rose in price, with two unchanged and eight falling. The largest monthly price increases were seen in motor fuel, audio discs and tapes, and internet services, with the largest declines among video purchase and rental subscriptions, cable satellites and streaming services, and postage/delivery services.

AIER Everyday Price Index vs. US Consumer Price Index (NSA, 1987 = 100)

(Source: Bloomberg Finance, LP)

{kind=link}

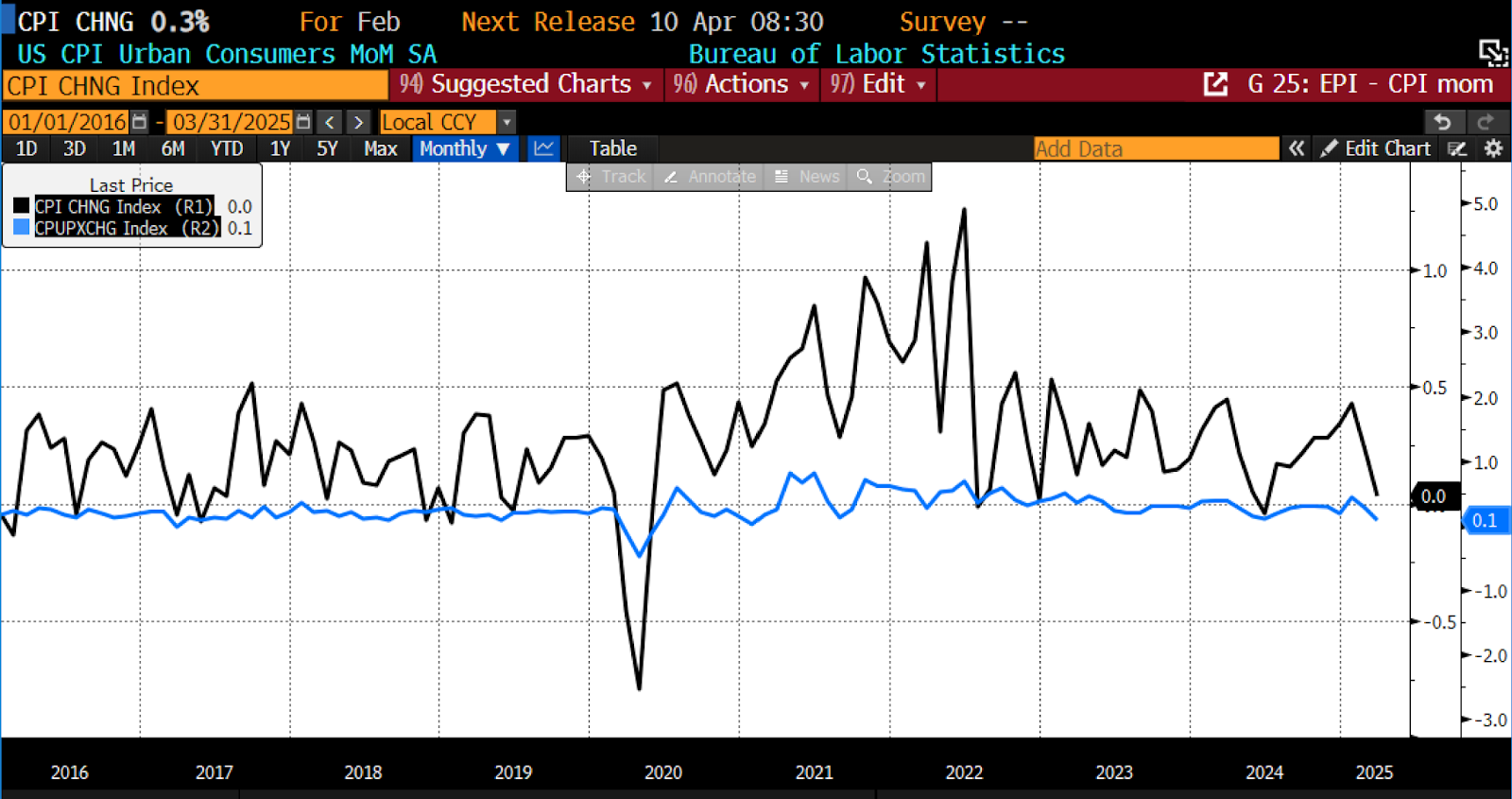

The US Bureau of Labor Statistics (BLS) released the February 2026 Consumer Price Index (CPI) data on March 11, 2026. From January to February 2026, headline CPI increased by 0.3 percent and core rose 0.2 percent; both were in line with forecasts.

February 2026 US CPI headline and core month-over-month (2016 – present)

(Source: Bloomberg Finance, LP)

{kind=link}

Consumer prices in February were driven primarily by shelter and a modest firming in energy and food costs, with the index excluding food and energy increasing 0.2 percent for the month. Shelter was the largest contributor to the overall increase, while gains were also recorded across several service and discretionary categories including medical care, apparel, household furnishings and operations, airline fares, and education. Within medical care, hospital services and physicians’ services moved higher even as prescription drug prices declined slightly. Offsetting some of these increases were declines in communication services, used cars and trucks, motor vehicle insurance, and personal care, suggesting continued easing in selected consumer goods and insurance-related categories.

Food prices rose 0.4 percent in February, matching the increase in the food-at-home index and following smaller gains in January. Grocery price movements were mixed: fruits and vegetables and nonalcoholic beverages both moved higher, while the “other food at home” category posted a notable increase driven in part by a sharp rise in candy and chewing gum prices. In contrast, dairy products declined, led by lower cheese prices, while cereals and bakery products edged down and the meats, poultry, fish, and eggs category was unchanged overall. Prices for meals away from home increased 0.3 percent as both limited-service and full-service meals became modestly more expensive. Energy prices also turned higher in February, rising 0.6 percent after January’s decline, reflecting increases in gasoline and natural gas prices that were partly offset by a drop in electricity costs. Overall, February’s inflation profile reflected moderate increases across housing, food, and selected services alongside pockets of softness in vehicles, insurance, and communications.

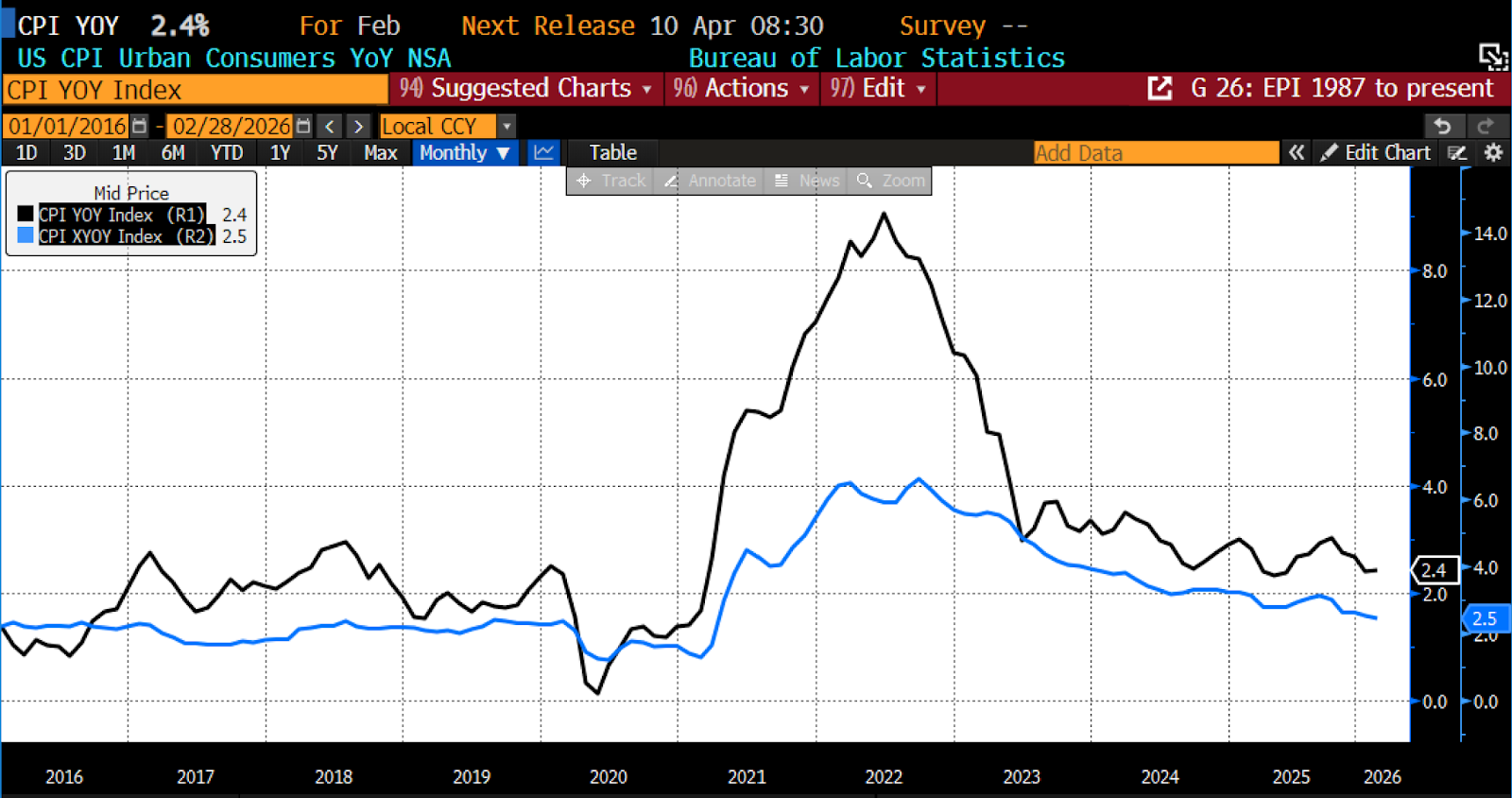

On the year-to-year side, headline CPI rose 2.4 percent, which was in line with forecasts. Core year-over-year inflation also met surveyed expectations of 2.5 percent.

February 2026 US CPI headline and core year-over-year (2016 – present)

(Source: Bloomberg Finance, LP)

{kind=link}

From February 2025 to February 2026, overall consumer prices increased 2.4 percent, unchanged from the pace recorded in January, while core inflation — excluding food and energy — rose 2.5 percent over the year. Food prices continued to show steady upward pressure, rising 3.1 percent over the past year, with grocery prices up 2.4 percent. Within grocery categories, nonalcoholic beverages recorded one of the largest increases, climbing 5.6 percent, while fruits and vegetables and cereals and bakery products each advanced 2.7 percent. The “other food at home” category rose 3.3 percent, while meats, poultry, fish, and eggs edged up 0.4 percent despite a sharp decline in egg prices. Dairy products posted only a slight 0.1 percent increase. Dining out remained a notable contributor to food inflation, with the food away from home index rising 3.9 percent over the year, driven by a 4.6 percent increase in full-service meals and a 3.2 percent rise in limited-service meals.

Energy prices increased modestly over the year, rising 0.5 percent overall as declines in gasoline prices offset gains in other components. Gasoline prices fell 5.6 percent over the 12-month period, while electricity costs rose 4.8 percent and natural gas prices increased a notable 10.9 percent. Excluding food and energy, core consumer prices increased 2.5 percent over the year, with shelter costs advancing 3.0 percent and continuing to anchor underlying inflation. Additional upward pressure came from medical care, household furnishings and operations, recreation, and personal care ( the latter posting a 4.5 percent increase) highlighting continued firmness across several service and household-related categories, with energy prices remaining relatively subdued.

February’s inflation report pointed to a continued easing in underlying price pressures, with core consumer prices rising 0.2 percent on the month and holding at 2.5 percent year-over-year — the slowest pace in nearly five years. The moderation reflected softer housing costs and ongoing declines in categories such as used vehicles and motor vehicle insurance, while goods prices excluding food and energy barely moved overall. Still, the details revealed a complex mix of offsetting forces. Apparel prices rose sharply, some electronics and recreation-related goods saw increases linked to rising metals and semiconductor costs, and certain discretionary services — including air travel, hotels, and car rentals — continued to post gains. At the same time, rents and owner-equivalent rents advanced only modestly, suggesting that one of the largest contributors to inflation over the past several years may be gradually cooling. Food inflation ticked higher in February, driven in part by rising fruit and vegetable prices, even as egg prices continued to retreat from last year’s historic spike.

Beneath the headline moderation, however, the data also hinted at emerging pressures that could complicate the outlook. Energy prices turned higher during the month, with gasoline and natural gas contributing modestly to the overall increase. Meanwhile, supply shocks in metals and electronic components have begun to filter into some consumer goods prices, particularly in recreation items and technology products. Price increases were also less pervasive across the core CPI basket than in January, reflecting the typical seasonal pattern in which businesses implement many of their annual price adjustments early in the year.

Still, the overall picture suggests inflation pressures are shifting rather than disappearing. If geopolitical tensions remain contained, moderating rent growth and cooling goods prices could leave room for the Federal Reserve to consider rate cuts later this year. But the war against Iran, now entering its second week — and the resulting surge in oil, natural gas, gasoline, and fertilizer prices — could quickly complicate that calculus by pushing headline inflation higher.

Even as overall inflation cools, the cost of everyday staples continues to weigh on household budgets, underscoring how affordability pressures persist despite improving macroeconomic indicators. Coffee prices provide a vivid example, and in their ubiquity a counterpart to gasoline prices at the pump. US retail coffee prices reached a record $9.46 per pound in February, up 31 percent from a year earlier, reflecting earlier supply disruptions in Brazil and Vietnam as well as tariff-related costs that continue to filter through the supply chain. Because coffee beans purchased months ago at elevated prices are still working their way through inventories, consumers may not see meaningful relief until well into 2027. Similar dynamics are evident in other grocery items and prepared beverages, where retail prices remain elevated even as underlying commodity markets soften.

Looking ahead, the developing war introduces a significant new risk of higher prices. Oil has already surged since the outbreak of hostilities, and the resulting increases in gasoline, energy, and transportation-related costs are likely to show up prominently in the March CPI report scheduled for release on Friday, April 10. As a result, February’s comparatively mild inflation reading may prove to be a brief lull before a new round of price pressures, these largely relating to energy, emerge in the months ahead.