{kind=link}

The strains emerging in the roughly $3 trillion private credit market are no longer isolated anecdotes; they are coalescing into a coherent signal of tightening financial conditions at precisely the wrong moment for the broader economy.

As discussed previously, a growing list of developments has unsettled investors. Now, on top of those at Blue Owl Capital, Apollo Global Management, and Morgan Stanley’s North Haven Private Income Fund, JPMorgan Chase has begun marking down private credit loans. Concerns have gone international. These are not systemic failures, but they do mark the transition of private credit from a benign, yield-enhancing allocation into a market experiencing its first meaningful credit cycle. The sector, which expanded rapidly after the Global Financial Crisis as banks retreated from riskier lending, now faces the test of higher rates, weaker borrower fundamentals, and more discerning capital.

It is critical to mention (or reiterate) that this is not shaping up as a 2008-style solvency crisis. The private credit market is small, leverage is generally lower, and there is little evidence of the kind of widespread fraud or securitization opacity that defined the subprime mortgage crisis. But that comparison risks missing a more relevant dynamic: private credit is a tightening mechanism. Its problems do not need to trigger bank failures to matter. Instead, they transmit stress through funding channels, into refinancing constraints, and ultimately into valuation pressure. Banks’ exposure — variously estimated from under $100 billion to potentially near $1 trillion globally when commitments are included — creates a feedback loop whereby losses or even perceived risks in private credit lead to tighter lending standards broadly. The nature of that tightening is not to remain contained; it ripples outward to impact middle-market firms, consumer borrowing, and ultimately, aggregate demand.

The mechanics of that tightening are already visible. Higher yields increase borrowing costs directly, but they also operate indirectly by raising discount rates, lowering asset valuations, and making refinancing more difficult. Private credit funds, often reliant on bank revolvers and leverage to enhance returns, become more fragile as funding costs rise. Borrowers — especially highly leveraged, floating-rate borrowers such as software firms — face a double bind of rising debt service burdens and deteriorating business prospects, particularly in sectors now facing disruption from generative AI.

Estimates that 15 percent to 25 percent of private credit portfolios are exposed to such firms underscore the vulnerability, with some projections suggesting default rates could approach eight percent in stressed scenarios. Even absent widespread defaults, the marginal borrower is already being shut out, and that is the entire point: credit availability is shrinking.

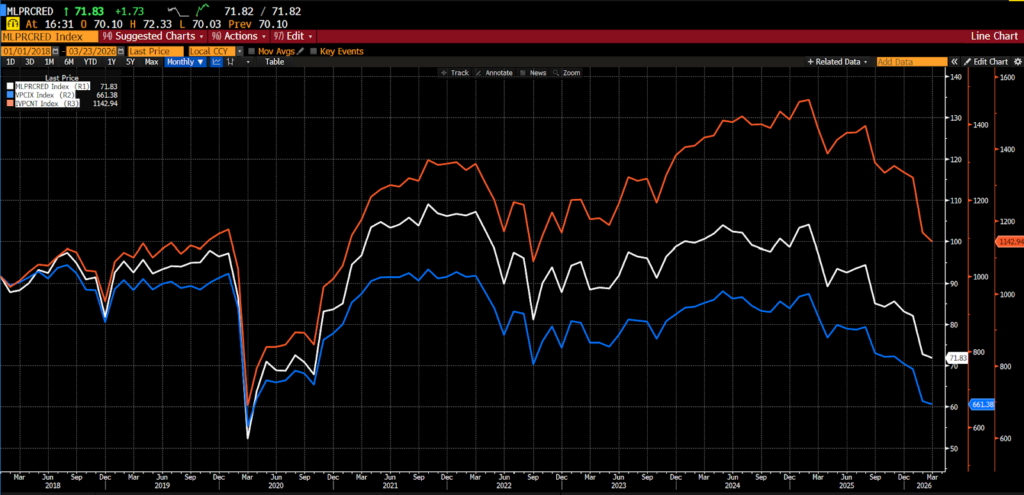

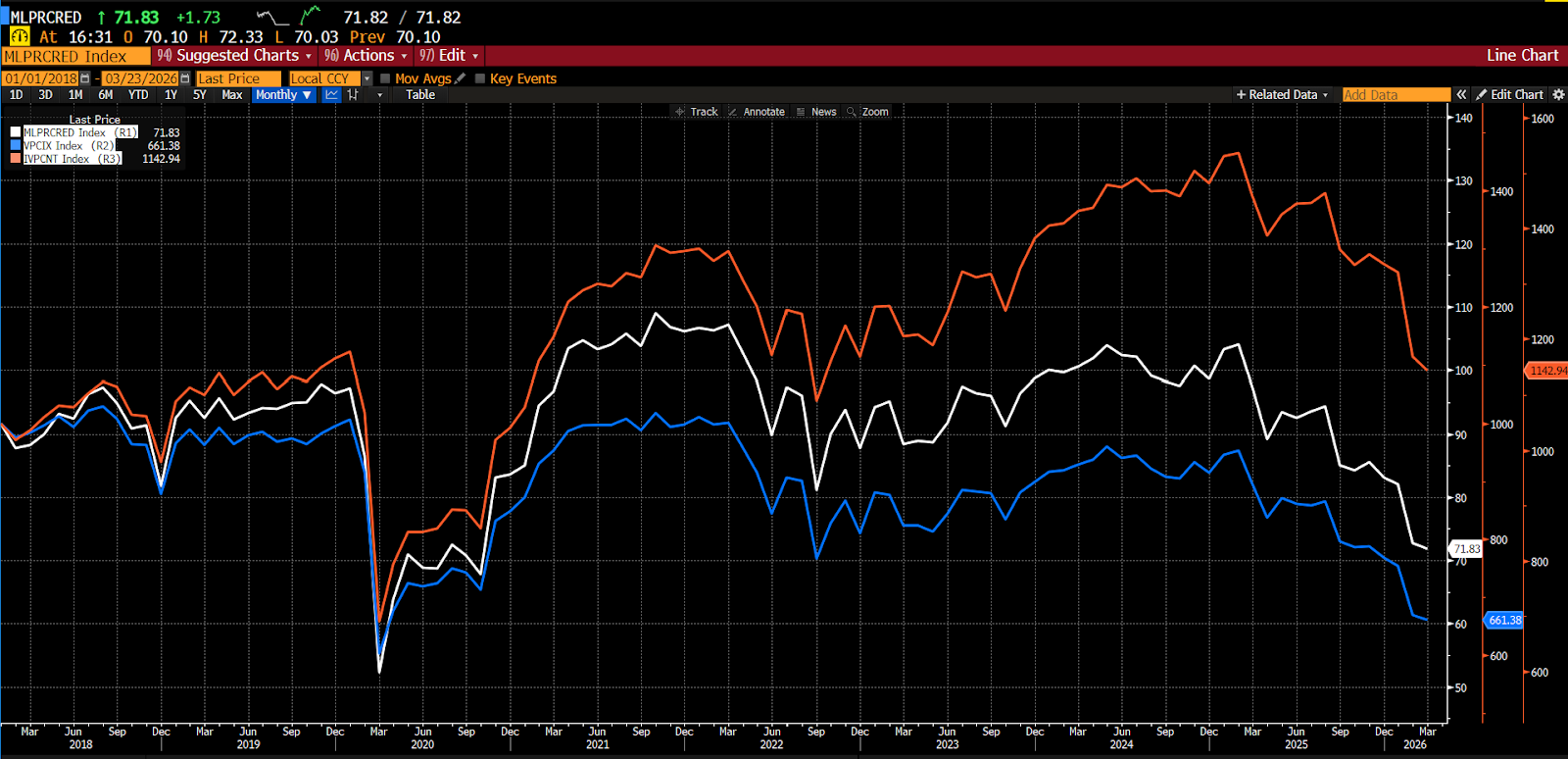

Bank of America Private Credit Proxy (white), VettaFi Private Credit Index (blue), and Indxx Private Credit Index (orange), 2018–present

(Source: Bloomberg Finance, LP)

{kind=link}

This tightening is unfolding against an increasingly unfavorable macro backdrop. Energy prices are rising, renewing inflationary pressure into an environment where disinflation had only recently begun to take hold. At the same time, yields across the curve have been moving higher, reflecting both inflation concerns and increased term premia. Rate futures markets, which had priced a steady path of easing, are now assigning a small but meaningful probability that policy rates could end the year higher rather than lower. That shift matters disproportionately for private credit, where floating rate structures and short-duration funding expose both lenders and borrowers to immediate changes in financing conditions.

The result is a reinforcing cycle. Higher energy prices push inflation expectations upward, keeping central banks cautious. That sustains higher yields, which tighten financial conditions directly and through channels like private credit. As private credit funds pull back, mark down assets, or restrict redemptions, confidence weakens and liquidity becomes more selective. This, in turn, constrains investment and hiring among other companies, but in some cases, the very firms that have come to depend on private lending. It is a quieter, more diffuse form of stress than in 2008, but consequential nevertheless.

Two factors are making the current moment particularly delicate. The first is that pressures are converging rather than offsetting. In prior cycles, falling energy prices or relaxing yields might have cushioned a credit tightening episode. Today, the opposite is occurring: energy, rates, and credit conditions are all moving in a direction that arrests growth. Private credit is not the epicenter of a crisis, but it is an increasingly important transmission channel through which macro tightening is being amplified.

The second is how much remains unknown. There is no centralized reporting, and visibility into indirect exposures is limited. In fact, there is no consistent definition of what the concept of private credit as an asset class ultimately encompasses. Also unclear is where the risks ultimately reside: would losses stay within private credit vehicles, migrate onto bank balance sheets, or into retail portfolios, pensions, and insurance structures that may not fully disclose their exposure? While the situation does not threaten a “Lehman moment” in scale or leverage, the lack of transparency means policymakers and analysts cannot confidently assess whether stresses will remain contained or propagate through tightening credit conditions, making the key risk not what is visible, but what remains hidden.

The emerging strains in private credit should be understood less as a harbinger of systemic collapse and more as an early indicator of economic deceleration. The asset class is doing what credit markets ultimately do in late-cycle conditions: becoming more selective, much more expensive, and far less forgiving. While far from inevitable, that process, especially when synchronized with rising input costs and a shifting rate outlook, is unlikely to be benign.